Will bankruptcy take my home equity?

Mia Lopez

Mia Lopez

Home equity is considered an asset in your bankruptcy. In Chapter 13 bankruptcy, you must pay the value of your nonexempt assets to your unsecured creditors through your repayment plan. As a result, the amount of equity you have in your home can play an essential role in your decision to file for bankruptcy.

Is it better to pay off credit card debt before buying a house?

Generally, it’s a good idea to fully pay off your credit card debt before applying for a real estate loan. This is because of something known as your debt-to-income ratio (D.T.I.), which is one of the many factors that lenders review before approving you for a mortgage.

What are the potential problems of misusing the home equity loan?

The main risks of a home equity loan are: Interest rates can rise with some loans. Your home is on the line. Equity can rise and fall. Paying the minimum could make payments unmanageable down the line.

Can I keep my house in Chapter 7 if I have equity?

Most Chapter 7 bankruptcy filers can keep a home if they’re current on their mortgage payments and they don’t have much equity. However, it’s likely that a debtor will lose the home in a Chapter 7 bankruptcy if there’s significant equity that the trustee can use to pay creditors.

How much equity can I keep in bankruptcy?

If you use System 1 bankruptcy exemptions, you may be able to exempt from $75,000 to $175,000 of your home’s equity. Basically, if California’s bankruptcy exemptions eat up enough of your home’s equity value, the court’s trustee may not sell it off to pay your creditors.

How much credit card debt is too much for a mortgage loan?

If your DTI is higher than 43%, you’ll have a hard time getting a mortgage. Most lenders say a DTI of 36% is acceptable, but they want to loan you money so they’re willing to cut some slack. Many financial advisors say a DTI higher than 35% means you are carrying too much debt.

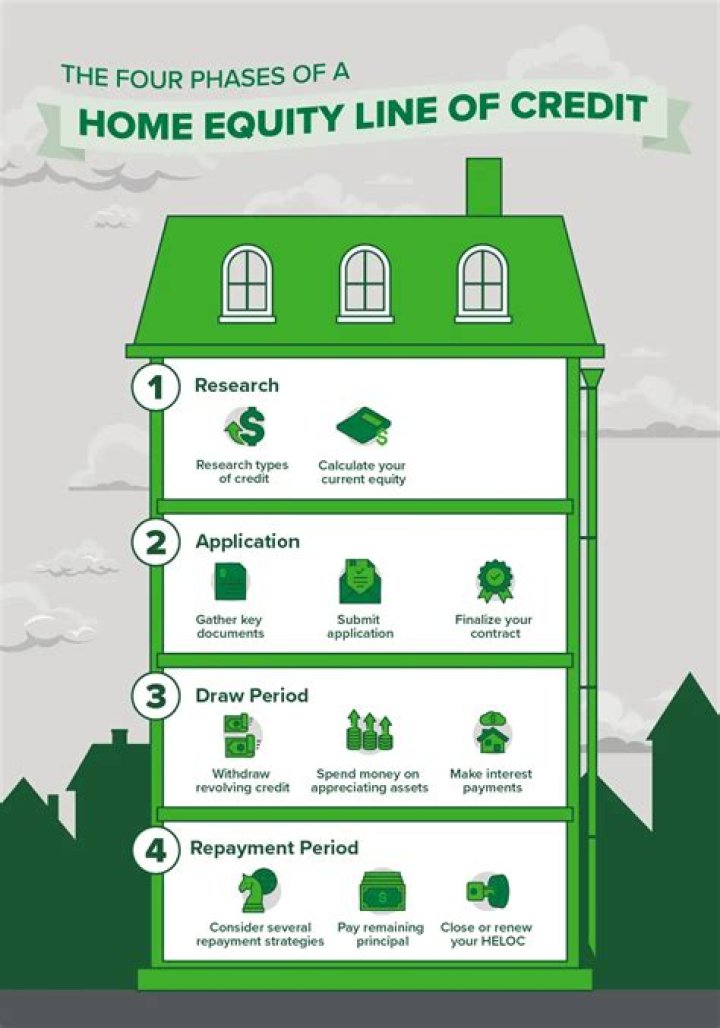

What is the debt to income ratio for a home equity loan?

Requirements for borrowing against home equity vary by lender, but these standards are typical: Equity in your home of at least 15% to 20% of its value, which is determined by an appraisal. Debt-to-income ratio of 43%, or possibly up to 50% Credit score of 620 or higher.

What can happen if you are unable to pay back an equity loan?

Defaulting on a home equity loan or HELOC could result in foreclosure. If you have equity in your home, your lender will likely initiate foreclosure, because it has a decent chance of recovering some of its money after the first mortgage is paid off.

Which is better, bankruptcy or a lien on your home?

However, if you owe $15,000, $20,000 or even more in credit card debt, bankruptcy could be a better option. You could spend as little as $500 and have all that credit card debt dismissed in six months or less. This would give you a fresh start, which could be much better in the long run than having your wages garnished or a lien put on your home.

Can you get a home equity loan while in bankruptcy?

Unfortunately, you would not be able to get a home equity loan while in Chapter 7 bankruptcy for a number of reasons. Your assets are largely controlled by the bankruptcy court. When you borrowed money to buy your home, you signed a note (which is the loan) and a mortgage (which is the lien).

Can you file for bankruptcy if you have credit card debt?

Yes, Chapter 7 bankruptcy erases almost all credit card debt. So, if you owe far more than you think you can pay, Chapter 7 can likely help you get back on your feet and stay there.

Which is better a Chapter 7 bankruptcy or a personal bankruptcy?

The biggest plus of a bankruptcy is that it will dismiss most of your unsecured debts. This means it will eliminate all your credit card debts, medical bills, and personal loans. The idea behind a chapter 7 is to give you a “fresh start”.