Why would a credit card company lower my credit limit?

James Rogers

James Rogers

A credit limit decrease can happen because your spending habits changed or if your good credit is mixed up with someone else’s bad credit. A sudden decrease in your credit limit can hit when you least expect it, curbing your buying power and potentially lowering your credit score, but you don’t have to let it stand.

Will lowering my credit limit hurt my credit?

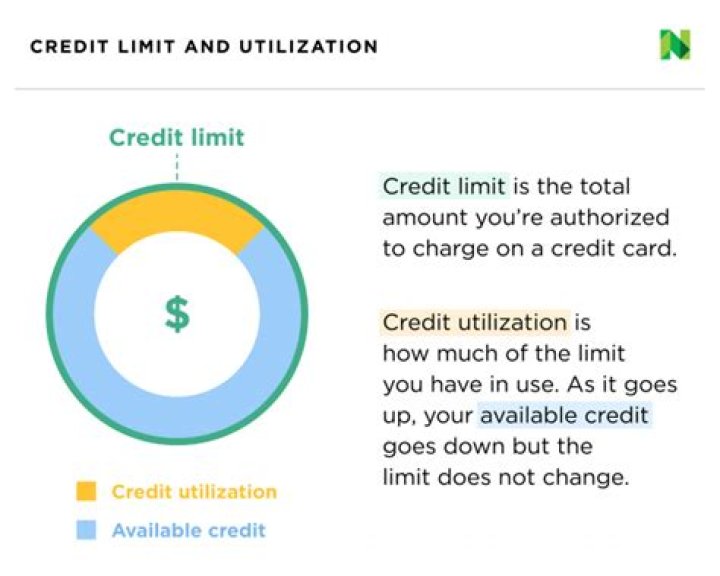

Lowering your credit limit can actually hurt your credit scores. The reason is that doing so increases your overall balance to limit ratio, or utilization rate. The lower your utilization rate, the less risk you represent to lenders. Therefore, it hurts your credit scores.

How do you get your credit card limit lowered?

How to reduce your credit limit in 5 steps

- Find out what your current credit limit is.

- Determine your current balance on the account.

- Make a calculated decision regarding how much you want to lower your line of credit.

- Contact the lender.

- Opt-out of any automatic account review programs.

Why did synchrony lower my credit limit?

It’s likely that Synchrony Bank lowered your credit limit because your recent credit history may show that you’re a higher-risk customer than you were in the past. If you’d like to get your limit raised, aim to lower your credit utilization and work on making minimum payments on-time every month.

Is it good to have high credit limits?

Increasing your credit limit can lower credit utilization, potentially boosting your credit score. A credit score is an important metric lenders use to determine a borrower’s ability to repay. A higher credit limit can also be an efficient way to make large purchases and provide a source of emergency funds.

What happens if my credit card issuer reduces my credit limit?

If a card issuer decreases your credit limit, the card issuer cannot charge you over-the-limit fees or a penalty rate for exceeding your new, lower credit limit, until 45 days after it has given you notice of the decreased credit limit.

What to do when your credit limit goes down?

If you normally use a large part of your available credit, a lower limit may have a bigger impact. One strategy to offset the impact is to get a new balance transfer card and transfer all or part of your balance from your existing card to your new one. For example, suppose you have one card with a $5,000 limit.

Can a credit card company charge an over the limit fee?

Under the law, your issuer is prohibited from charging an over-the-limit fee within 45 days of the credit limit decrease if it leaves your balance higher than the new limit. But it’s rare that an issuer would reduce your limit to less than what you’ve already charged with your card.

Why is it important to have a credit limit?

Credit limits exist for good reason. Your card company doesn’t want you to charge more than you can afford to repay, and you don’t want that to happen either. Your limit is a safeguard of sorts for both you and your card company. Your credit limit is also an important factor in your credit utilization ratio, which influences your credit scores.