Why is the provision for doubtful debts created?

James Rogers

James Rogers

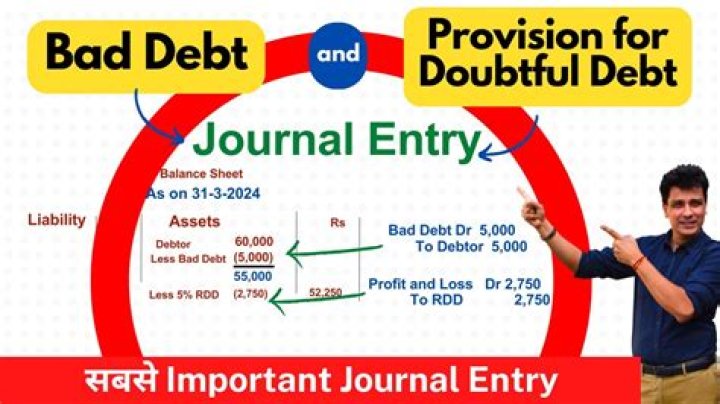

The provision for doubtful debt account is created to reduce the accounts receivable balance to its net realizable value without having to credit it. Since it is a contra asset account it has a credit balance as compared to the debit balance of accounts receivable.

Why is doubtful debt important?

Why is doubtful debt important? It’s important to be aware of – and account for – doubtful debt so that you can protect your company’s financial health. Most businesses provide goods or services on credit, which creates ‘credit risk’ – the risk that some customers may not pay either some or all of what they owe.

Is doubtful debt an expense?

Doubtful debts or bad debts is an expense and has already occurred. The provision is a future loss – a future loss that must be recorded as soon as it becomes likely to occur. So you record the loss (expense account) called doubtful debts or bad debts for the amount of $500.

Why is provision for doubtful debts created how it is shown in balance?

This is because the Provision for Doubtful Debts is created only on doubtful debts and not on Bad Debts. The amounts of bad debts and new provision for doubtful debts are deducted from the Sundry Debtors on the asset side of the Balance Sheet.

When is a doubtful debt considered a liability?

Sort of. So it is considered a liability. But a special type of liability. In other words, doubtful debts or bad debts have already occurred – the debt is bad right now. For example, Joe Shmoe (debtor) owed you $500 and he just told you he is filing for bankruptcy and can’t pay anything.

Is the allowance for bad debts an asset or liability?

Similarly, the accumulated allowance for bad debts is subtracted from debtors to give us the Net collectable debts. So I would venture to say the allowance for bad debts is, in fact, a negative asset and not a liability. IFRS 9 chooses the term allowance for bad debts not provision for bad debts.

How are bad debts classified on a balance sheet?

In the Balance sheet, the accumulated depreciation is subtracted from cost to give the Net Book Value of the Non-current asset. Similarly, the accumulated allowance for bad debts is subtracted from debtors to give us the Net collectable debts.