What is usually required for a down payment on a house?

Emily Carr

Emily Carr

20%

The traditional advice is to make a down payment of at least 20% of your new home’s value. This is a great benchmark to aim for because it will get you more favorable loan terms and you won’t have to pay PMI. However, most homebuyers make down payments of 6% or less. This is especially true for first-time homebuyers.

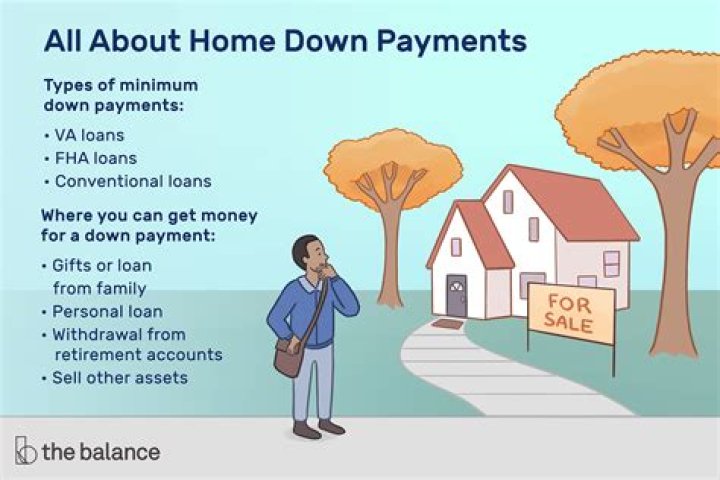

Can you take a loan for a downpayment on a house?

The short answer is: probably not. You likely won’t find many options for a down payment loan — which is a personal loan that you use to make a down payment on a home. And those that do exist come with some drawbacks. Instead, you may have better luck looking for a mortgage that doesn’t require a 20% down payment.

Can I borrow for a down payment?

Pros and cons of tapping home equity for a down payment You can borrow up to 85% of your current home’s value. You may have to pay closing costs of 2% to 5% of the loan amount. You may avoid private mortgage insurance (PMI) on your new home with a 20% down payment. You’ll have to qualify with two mortgage payments.

What house can I afford on 30k a year?

If you were to use the 28% rule, you could afford a monthly mortgage payment of $700 a month on a yearly income of $30,000. Another guideline to follow is your home should cost no more than 2.5 to 3 times your yearly salary, which means if you make $30,000 a year, your maximum budget should be $90,000.

Do you have to have a down payment on a home?

Many people would take out two loans in order to avoid the cost of private mortgage insurance (PMI) and still not have a down payment on their home. Some banks also offer 100 percent financing for a home. Other couples may qualify for an FHA loan, which eliminates the need for a large down payment.

What’s the best amount to put down for a home loan?

Iowa-based entrepreneur Richard Dedor and his husband put down between $20,000-25,000, which was right around 10% of their home cost, in order to position their mortgage payment in a certain financial range. “We basically saved as much as we could, as we knew what we needed our monthly mortgage payment to be in the end,” he says.

Do you have to put down money for a second home?

You’ll likely have to put 10% to 20% down up front, depending on your lender and credit profile. But even if you don’t have a huge amount of cash savings on hand, that doesn’t mean you can’t purchase a second home — you can borrow money for you down payment, too.

How big of a down payment do I need to buy land?

If you’re in the market for raw land, expect to make a much larger down payment than you would on improved property, such as a lot with a house. Down payments for land loans generally range between 20 and 50 percent of the purchase price.