What is the difference between provision for bad debts and provision for doubtful debts?

Emily Carr

Emily Carr

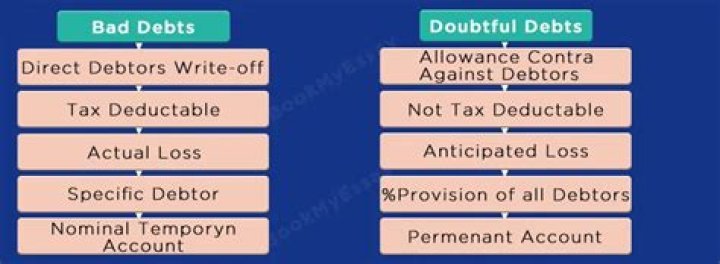

Provision for bad debts meaning The provision for doubtful debts, which is also referred to as the provision for bad debts or the provision for losses on accounts receivable, is an estimation of the amount of doubtful debt that will need to be written off during a given period.

How do you determine bad and doubtful debts?

The basic method for calculating the percentage of bad debt is quite simple. Divide the amount of bad debt by the total accounts receivable for a period, and multiply by 100. There are two main methods companies can use to calculate their bad debts.

What account is doubtful debts?

The provision for doubtful debts is an accounts receivable contra account, so it should always have a credit balance, and is listed in the balance sheet directly below the accounts receivable line item. The two line items can be combined for reporting purposes to arrive at a net receivables figure.

Are doubtful debts liabilities?

Provision for doubtful debts, on its own, would technically be considered a current liability account, as it is the estimate of debts that will occur in the next year. “Trade and other receivables” is your net debtors.

What’s the difference between book debts and doubtful debts?

Hence there will be a number of border line cases in which there will be an element of doubt regarding the realization of the debts. Those book debts will be termed as Doubtful Debts. However similar they may sound, there is difference between bad and doubtful debts.

What’s the difference between a doubtful debt and a credit memo?

The first alternative for creating a credit memo is called the direct write off method, while the second alternative is called the allowance method for doubtful accounts. A doubtful debt is an account receivable that might become a bad debt at some point in the future.

When do you debit or credit a bad debt?

Accounting for a Bad Debt When you create the credit memo, credit the accounts receivable account and debit either the bad debt expense account (if there is no reserve set up for bad debts) or the allowance for doubtful accounts (which is a reserve account that is set up in anticipation of bad debts).

When do you write off a bad debt?

The debit in the transaction is to the bad debt expense. When you eventually identify an actual bad debt, write it off (as described above for a bad debt) by debiting the allowance for doubtful accounts and crediting the accounts receivable account. Example of a Bad Debt and Doubtful Debt