What information is not used to calculate your credit score?

James Rogers

James Rogers

The following information is not considered in determining your credit score, according to FICO: Marital status. Age (though FICO says some other types of scores may consider this)

What is the most commonly used credit scoring model?

FICO Scores

FICO Scores According to FICO, their scores are used in more than 90% of lending decisions, making them the most widely used type of credit score in the industry.

What is credit scoring model?

A credit scoring model is a mathematical model used to estimate the probability of default, which is the probability that customers may trigger a credit event (i.e. bankruptcy, obligation default, failure to pay, and cross-default events). The higher score refers to a lower probability of default.

How is your credit score calculated from your credit report?

The score generally ranges from 300-850 and is calculated using credit history information from your credit report. Your accounts, payment history, and inquiries into your credit are examples of credit report information used to calculate your credit score. 1 How Your Credit Score Is Used

How is payment history used to calculate credit score?

Even though the specific equation for coming up with your credit score is proprietary information owned by FICO, we do know what information is used to calculate your score. 5 Payment history: Lenders are most concerned about whether or not you pay your bills on time. The best indicator of this is how you’ve paid your bills in the past.

What should be included in a credit score?

Revolving credit (credit cards, retail store cards, gas station cards, lines of credit) and installment credit (mortgages, auto loans, student loans) should both be represented, if possible. 9 It is important to understand that your credit score reflects only the information contained in your credit report.

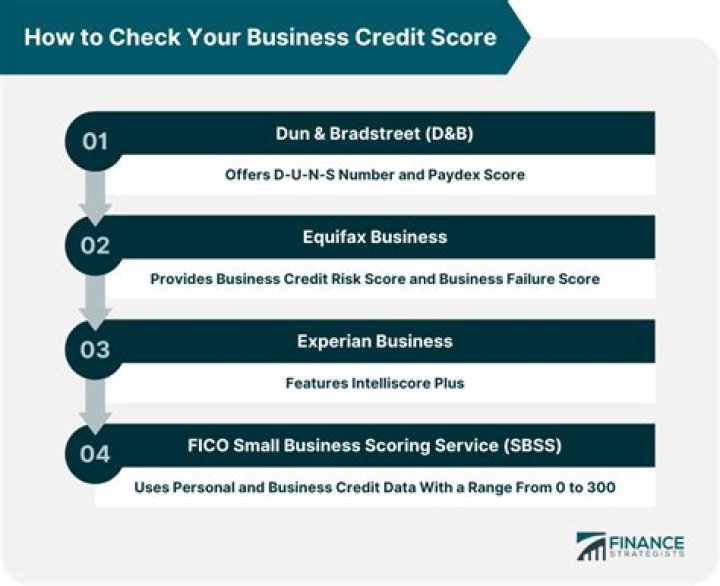

How are credit scores calculated according to Equifax?

1 The number of accounts you have 2 The types of accounts 3 Your used credit vs. your available credit 4 The length of your credit history 5 Your payment history