What happens to my student loans if I file bankruptcy?

William Brown

William Brown

If you are currently in school, your federal student loans should not be an issue as they probably in a grace period. Defaulting on your student loans can lead to denial of future federal loans. PLUS loan eligibility could be affect by a bankruptcy filing.

Is it possible to get rid of student loan debt?

And bankruptcy can be a way to get help. Bankruptcy is not fun. Your credit gets destroyed for years, and you have to be in pretty dire financial straits for it to make sense. But if you reach that point, you can get your debts reduced or erased through bankruptcy so you can get back on your feet.

Can you go back to school after bankruptcy?

If you are attending school or plan on attending school after filing for bankruptcy, you should consult with lenders and your school’s financial aid department to discuss your options if you are relying on private loans. Private student loans should be taken out only when absolutely necessary and for the minimal amount.

Can you get federal financial aid if you file bankruptcy?

§ 525 (c) 1 You can’t be denied federal financial aid because you’ve filed bankruptcy in the past. 2 Government student aid providers can’t hold nonpayment of a dischargeable (or discharged) debt against you. 3 You can get federal loans while in Chapter 7 bankruptcy.

Can a parent get a PLUS loan if they file bankruptcy?

A PLUS loan is a type of federal loan available to graduate students and parents of dependent undergraduate students. A bankruptcy, or adverse credit history in general, may affect a parent’s chances of obtaining a PLUS loan for their dependent undergraduate student.

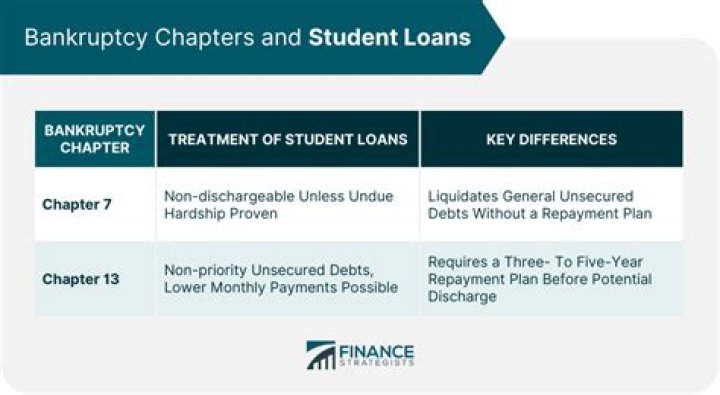

If, as in most cases, your loans are not discharged in bankruptcy, here’s what happens. Chapter 7 bankruptcy. In Chapter 7 bankruptcy, if payment of your loans is not an undue hardship, you’ll still owe them when your bankruptcy case is over. Chapter 13 bankruptcy.

When did student loans become nondischargeable in bankruptcy?

Thirty years later, Congress changed the U.S. Bankruptcy Code again to make some private loans nondischargeable absent undue hardship. Now, you can discharge your student loan debt only if you can show that paying back your loans will cause you or your dependents an undue hardship. When did student loans become nondischargeable in bankruptcy?

When to get rid of student loan debt?

The timing depends on the type of bankruptcy case you filed. For chapter 7 bankruptcy cases, you’ll typically start the process of getting rid of your student loans soon after you file bankruptcy. For chapter 13 bankruptcy cases, you’ll likely need to wait until your bankruptcy case is near the end.

Can a student get a loan from a bank?

However, private financial institutions, such as banks, also offer loans to students, primarily because many students cannot fund their entire education without such supplementation. It doesn’t matter whether you have a government or a private student loan.

Can you file an adversary proceeding after a Chapter 7 bankruptcy?

If you choose to file for Chapter 7, you can file the adversary proceeding right after filing your bankruptcy case. If you’ve already gone through Chapter 7 bankruptcy, and your case has been closed, you may still be able to file an adversary proceeding to get your student loans discharged.

What do I need to file for Chapter 7 bankruptcy?

To file Chapter 7, you must not have had another Chapter 7 bankruptcy discharged in the past eight years. Also, your current monthly income must fall below the state median or must pass a means test. 2 Certain debts cannot be discharged, such as taxes, alimony, and child support.

When do you file for student loan discharge?

Once your case is complete, you can file for student loan discharge. People turn to Chapter 13 bankruptcy when they can’t pass the Chapter 7 means test or don’t want to lose their home to foreclosure, which can happen if they have significant equity in the property.

Is it possible to discharge federal student loan debt?

Read less Bankruptcy is rarely an easy process, but it’s notoriously difficult with student loan debt. Though it is possible to discharge either federal or private student loans through bankruptcy, you have to prove undue hardship to do so.