What happens to HELOC in foreclosure?

Aria Murphy

Aria Murphy

After foreclosure, the equity you enjoyed in your property disappears along with your ability to make new purchases using your line of credit. This does not, however, exonerate you from your responsibility to repay any amount you previously charged using your HELOC.

Is a home equity loan risky because the lender can foreclose?

A home equity loan can be risky because the lender can foreclose if you don’t make your payments. However, in some states, the lender can not only take your home but continue to come after you if that home sale isn’t sufficient. If the home seizure doesn’t pay back the lender, the lender is out of luck.

Can a bank foreclose on a HELOC?

If you are unable to repay a loan that was secured by your home, such as a home equity line of credit, or HELOC loan, California law generally allows the lender to foreclose on your home to collect the loan.

What happens if you don’t pay your home equity line of credit?

Once you default on your home equity line of credit, your creditor can accelerate the repayment phase and cut off access to further funds. If you cannot repay, they can foreclose on your home or seek a court judgment against you.

Do HELOC loans expire?

HELOCs “Expire” After 10 Years, Usually The draw period typically lasts 10 years after which the remaining mortgage balance is recast to a fixed-rate loan at the prevailing market rate. The fixed-rate period typically lasts fifteen years. HELOCs are a revolving credit line.

Can a second mortgage foreclose if first is current?

A second-mortgage holder can initiate foreclosure proceedings even if the first mortgage is not behind on payments. The second-mortgage lender must still take all the necessary steps in the foreclosure process, and must also notify the first lender of the intention to foreclose on the property.

Can HELOC be forgiven?

In many cases, HELOCs that are forgiven or discharged by lenders are reportable as income from cancellation of the debt unless an exception to reporting applies.

How long does a home equity line of credit last?

10 years

A HELOC, on the other hand, is a line of credit that usually lasts 10 years. You can nibble away at it to pay for several, small home-improvement projects, or you can use it in big chunks to pay for a vacation or wedding. The interest rate on HELOCs is variable and you could take as long as 30 years to repay them.

Can a default on a HELOC cause foreclosure?

HELOCs and Defaults. HELOCs are line-of-equity loans secured by the homes their borrowers use as collateral for them. Because a HELOC borrower is pledging his home as security for his loan, the HELOC’s lender has a right to attach a lien to that home’s title.

What happens to a home equity loan after a foreclosure?

That’s because the first mortgage has priority, meaning that it’s likely that the home equity loan or HELOC holder will not receive any money after a foreclosure. Instead, the lender may choose to sue you personally for the money you owe.

What happens if you lose your home to foreclosure?

The very fact that you had equity in your home can prevent you from further legal consequences from your HELOC lender after losing your home to foreclosure. According to Texas A&M University, after foreclosure, your primary lender will sell your home and use the proceeds to pay off the amount due on your primary mortgage loan.

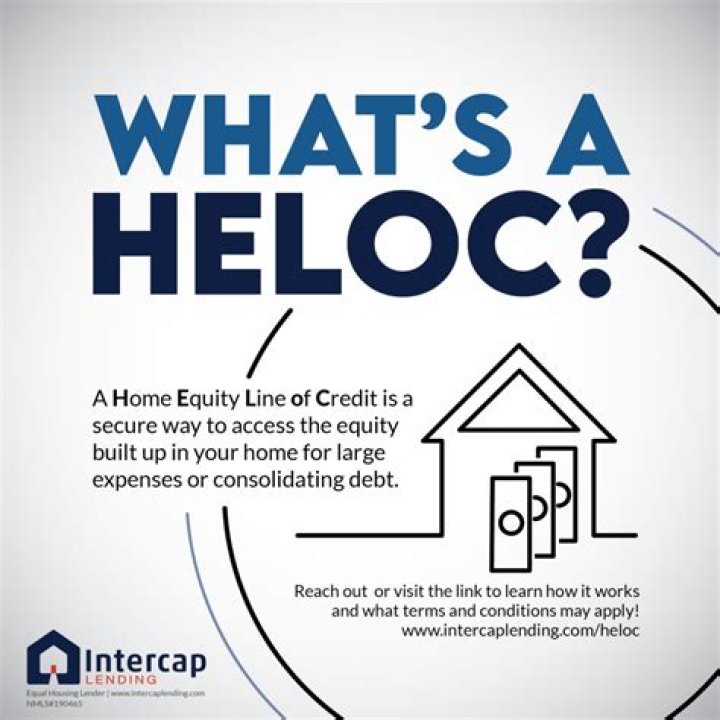

What’s the difference between a home equity loan and a HELOC?

The first is a loan of a set amount of money financed for a set period (usually five to 15 years) at a fixed interest rate and with a fixed payment. The second type is called a home equity line of credit (HELOC).