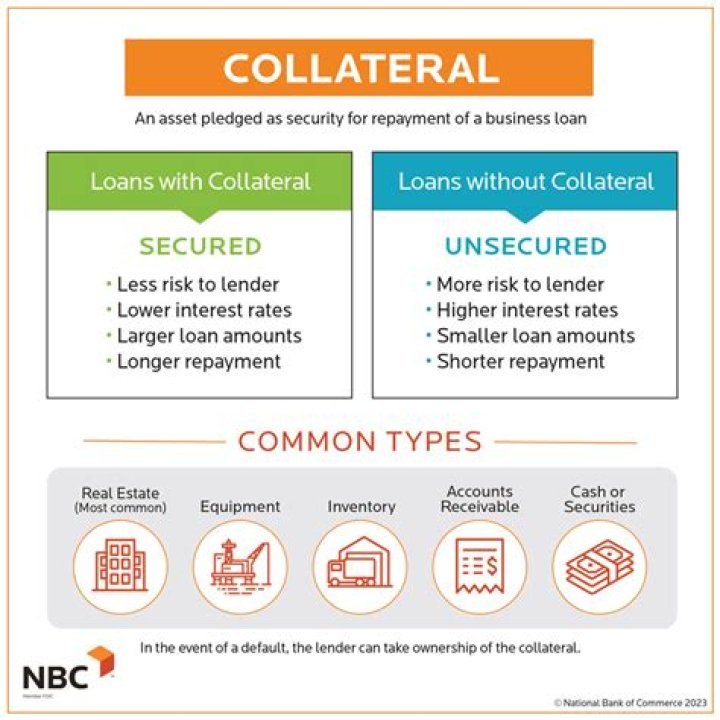

What happens to collateral in bankruptcy?

Emily Carr

Emily Carr

The lien on the property will survive your bankruptcy discharge. If the creditor fails to repossess the collateral, the lien on the collateral will still exist however, the creditor cannot try and collect money from you for the collateral after the bankruptcy is discharged.

Are all debts forgiven in Chapter 7 bankruptcy?

Chapter 7 Bankruptcy Discharge Wipes Out Most Debts Forever Most debts incurred by the typical American consumer are erased by Chapter 7. The types of debt Chapter 7 bankruptcy discharges are: credit card debt.

Can you file bankruptcy if you have a secured loan?

Secured debts are treated differently in Chapter 7 bankruptcy than other kinds of debts. Although the secured debt itself can be wiped out (discharged)—and often is—the creditor will still have a right to take the property back if you fail to pay (default on) the payments.

What happens to a debt in a Chapter 7 bankruptcy?

An individual receives a discharge for most of his or her debts in a chapter 7 bankruptcy case. A creditor may no longer initiate or continue any legal or other action against the debtor to collect a discharged debt. But not all of an individual’s debts are discharged in chapter 7.

Can a debtor be discharged under the Bankruptcy Code?

Not all debts are discharged. The debts discharged vary under each chapter of the Bankruptcy Code. Section 523 (a) of the Code specifically excepts various categories of debts from the discharge granted to individual debtors. Therefore, the debtor must still repay those debts after bankruptcy.

Why does collateral diminish in a bankruptcy case?

There are several reasons why the value of a secured creditor’s collateral might diminish during the course of a bankruptcy case. One reason is the debtor’s use of that collateral. For example, if your collateral is a new car, and the debtor, during the case, drives the car for a year and puts 15,000 miles on it, the value will be diminished.

Who are secured creditors in Chapter 11 bankruptcy?

The debtor, its equity-holders, managers, trade creditors, bondholders, bank lenders, customers, potential investors or acquirers, claims traders, the U.S. Trustee and even the judge each bring a unique set of perspectives, concerns and goals to a chapter 11 case. The secured creditor is no exception.