What happens if I file Chapter 7 bankruptcy and my spouse is not?

Mia Lopez

Mia Lopez

If you’re filing for Chapter 7 bankruptcy and your spouse is not, you may be wondering whether they are going to be affected. The short answer is that if your debts are separate, their credit will not be impacted.

Do you have to include your spouse’s income in your bankruptcy?

Answer. If the two of you share the same household, then yes. If you maintain separate households, then no. In both a Chapter 7 and Chapter 13 bankruptcy, you are required to include your spouse’s income in your bankruptcy petition. For a Chapter 7, her income must be included when doing the means test.

Can a married couple file for bankruptcy together?

Beyond just debt, another issue for married couples to consider when evaluating bankruptcy is property owned by the spouses. If one spouse owns property in their name only and is not the spouse filing bankruptcy, it generally won’t become part of the bankruptcy estate.

Is there an automatic stay for a non filing spouse?

Chapter 13 automatic stay. In Chapter 7, the automatic stay doesn’t protect a codebtor (or non-filing spouse) from creditor collection. The creditor can pursue whatever rights might exist against the non-filing spouse. In Chapter 13, the automatic stay covers codebtors as long as it remains in effect.

Do you have to include your spouse’s income in bankruptcy?

Including Your Spouse’s Income in Bankruptcy. If you want to take care of the debt by filing for bankruptcy, you’ll have to include your wife’s income if you share the same household—even if you file alone. Since your wife’s income is appreciable, it might affect your eligibility to receive a discharge in a Chapter 7 bankruptcy.

The issue comes up most frequently when only one spouse is planning to file for bankruptcy. Many have the mistaken impression that because they are married, their spouse is automatically responsible for their debts. This is not the case.

What happens to a husband’s credit when he files for bankruptcy?

When filing for bankruptcy, the bankruptcy filing will appear on the husband’s credit, but would not appear on the wife’s credit and there would be no adverse rating on her credit score because of the bankruptcy.

What happens to joint property in Chapter 7 bankruptcy?

This means that if you do not have enough exemptions to cover these assets, then they can be taken and sold by the Chapter 7 bankruptcy trustee to pay your creditors. Your spouse’s separate property and his or her share of joint property are not included in your bankruptcy.

Do you have to disclose your spouse in bankruptcy?

Just like common law states, the separate property of your spouse is not part of your bankruptcy. However, you may still be required to disclose it in your bankruptcy papers because the trustee may want to check and make sure it is, in fact, separate property.

Can a spouse be included in a bankruptcy estate?

However, in a community property state, all property acquired after the marriage will be included in the estate. Find out more about the assets of the bankruptcy estate. Sometimes the interests of spouses don’t align. For instance, a debtor’s separate property becomes part of the bankruptcy estate.

What happens to your property when you file bankruptcy?

When you file for bankruptcy, either alone or with your spouse, you may file under Chapter 7 or Chapter 13 of the Bankruptcy Code. If you file under Chapter 7, the bankruptcy trustee may take any of your property that is not exempt under the laws of your state (or the federal exemption laws, if your state allows you to use them).

Can you sell your house if you file Chapter 7 bankruptcy?

If you don’t have any equity, you’re in good shape—trustees don’t sell houses without equity. Otherwise, you’ll need to be able to protect your equity with a bankruptcy exemption to avoid losing the home in Chapter 7 bankruptcy.

Can You Lose Your Home if you file for bankruptcy?

State exemption statutes list the property its residents can protect in bankruptcy. Some states allow residents to choose between either the state exemption list or the federal bankruptcy exemption scheme. Either way, almost all states allow residents to protect some home equity with a homestead exemption.

Can a married couple file an individual bankruptcy?

An individual bankruptcy allows one spouse to wipe out his or her debts without negatively affecting the other spouse’s credit. Also, if your state doesn’t allow you to double your exemptions in a joint petition, you may be able to protect more of your property by filing two individual bankruptcies.

Can a spouse be included in a chapter 13 bankruptcy?

A non-filing spouse’s income must be included in a Chapter 13 case, even if the spouses live in two different homes. The filer might be able to offset the costs using the marital adjustment. Legal separation. Chapter 13 doesn’t distinguish between marriage and legal separation. A married debtor must include the income of the non-debtor spouse.

How often can you file a Chapter 7 bankruptcy?

Or, maybe you filed a Chapter 7 case years ago, received a discharge, but find yourself in financial difficulty again. Although you may have used a bankruptcy filing to get out of prior financial struggles, unfortunately, federal bankruptcy law does limit you on how often you can file a new case.

What happens to your credit if your ex spouse files for bankruptcy?

Joint or Cosigned Credit Obligations. If your ex-spouse files for bankruptcy, you will be responsible for the debt if you are a joint owner or cosigner. The lender can require you, as a joint owner or cosigner, to make payments on a loan if your ex-spouse declares bankruptcy on the credit.

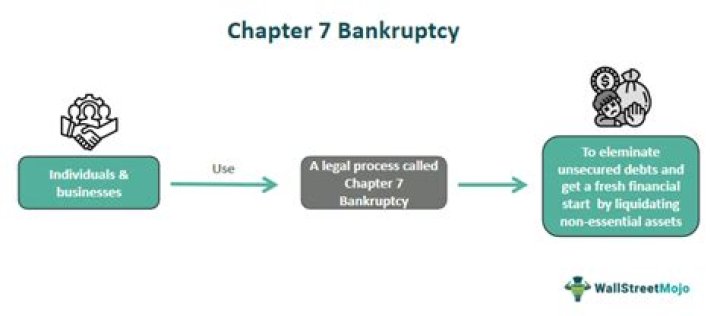

What kind of bankruptcy does an individual file?

Individual debtors can file for bankruptcy under Chapter 13 or Chapter 7 of the Bankruptcy Code. The U.S. Courts website explains that Chapter 13 bankruptcy is a repayment plan of debts over a period and that Chapter 7 bankruptcy eliminates—or discharges—most or all of the bills.

Can a trustee come after a spouse’s property in bankruptcy?

Debtors not located in one of these states generally do not have to worry about the trustee coming after their spouse’s property during a bankruptcy, even if the spouse owns property worth more than what the exemptions permit. Eva G. Bacevice graduated from the University of Michigan Law School in 2001.

Can a married couple file jointly for bankruptcy?

If one spouse owns many separate nonexempt assets—property a filer can’t protect with an exemption—it will be lost in Chapter 7 or need to be paid for through a Chapter 13 repayment plan. It might not make sense if filing jointly will put those assets at risk. The same logic applies if most debts are in the name of only one spouse.

What should I do if my husband went bankrupt?

If you’re already living together, you should go ahead and consult and attorney now to determine if it’s possible to commingle your property while keeping you out of his financial mess. If he still has significant debt post-bankruptcy, having this conversation with a lawyer is definitely worth your while.

Can a spouse file for bankruptcy in Texas?

However, in community property states like Texas, almost all assets acquired (and income earned) by either spouse during the marriage are considered community property. In other words, property acquired by either spouse during the marriage is considered equally the property of both spouses, a 50/50 split.

When is it better to file jointly or separately for bankruptcy?

If you and your spouse have separated and your spouse won’t cooperate, you may also have to file separately, even if a joint filing would be the better option. You own property together as tenants by the entirety, and your state excludes such property from the bankruptcy estate if only one spouse files alone.