What does your debt-to-income ratio need to be to buy a house?

Elijah King

Elijah King

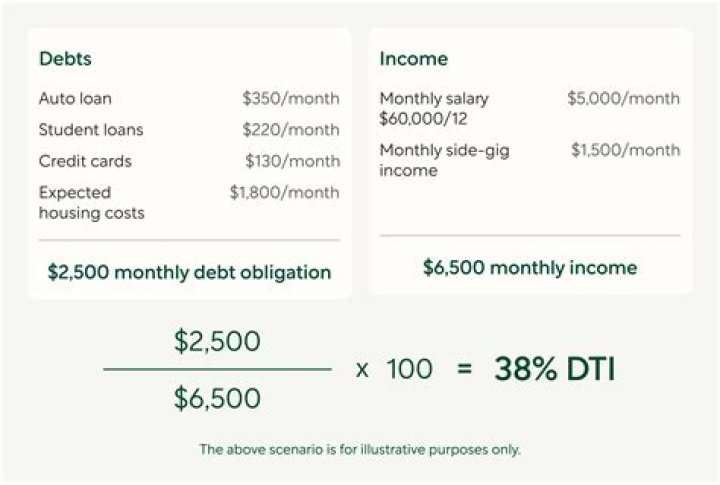

Lenders prefer to see a debt-to-income ratio smaller than 36%, with no more than 28% of that debt going towards servicing your mortgage. 12 For example, assume your gross income is $4,000 per month. The maximum amount for monthly mortgage-related payments at 28% would be $1,120 ($4,000 x 0.28 = $1,120).

How can I lower my debt-to-income ratio for a mortgage?

How to lower your debt-to-income ratio

- Increase the amount you pay monthly toward your debt. Extra payments can help lower your overall debt more quickly.

- Avoid taking on more debt.

- Postpone large purchases so you’re using less credit.

- Recalculate your debt-to-income ratio monthly to see if you’re making progress.

What should my debt-to-income ratio be for a car loan?

What is a good debt-to-income ratio? Lenders prefer to see DTI ratios below 36%, but there’s wiggle room. Research by rateGenius, a LendingTree partner, showed 90% of applicants approved for auto refinancing had a DTI of 48% or less.

How much house can you afford if you make 60000 a year?

The usual rule of thumb is that you can afford a mortgage two to 2.5 times your annual income. That’s a $120,000 to $150,000 mortgage at $60,000.

What happens if my debt-to-income ratio is too high?

Impact of a High Debt-to-Income Ratio A high debt-to-income ratio will make it tough to get approved for loans, especially a mortgage or auto loan. Lenders want to be sure you can afford to make your monthly loan payments. High debt payments are often a sign that a borrower would miss payments or default on the loan.

Can I buy a car with a high debt-to-income ratio?

Yes. The best ways to improve your DTI would be to pay down your monthly debt, increase your income, or do both. However, a high DTI ratio can mean the difference between getting a car loan and not getting one. So it’s wise to take care of your debts first, if possible, before applying for a car loan.

What is the max debt-to-income ratio for an FHA loan?

57%

FHA Loans. FHA loans are mortgages backed by the U.S. Federal Housing Administration. FHA loans have more lenient credit score requirements. The maximum DTI for FHA loans is 57%, although it’s lower in some cases.

How to calculate credit market debt to disposable income ratio?

To determine the credit-market debt to disposable income ratio for Country A, we add the credit-market debt across all households and divide it by the sum of disposable income across all households. The calculations are shown below: Total Credit-Market Debt = $250,000 + $450,000 + $30,000 + $150,000 + $650,000 = $1,530,000

How does a high debt to income ratio affect your credit?

Impact of a High Debt-to-Income Ratio. High debt payments are often a sign that a borrower would miss payments or default on the loan. While your credit score isn’t directly impacted by a high debt-to-income ratio, some of the factors that contribute to a high debt-to-income ratio could also hurt your credit score.

How can I lower my debt to income ratio?

In addition to lowering your debt, you can change your DTI by increasing your income. As described in the example above, someone who makes $2,000 each month and pays $1,000 toward loans has a 50% DTI. But if that monthly income increased to $3,000, then the DTI would go down to 33%.

How to improve your DTI and credit utilization ratio?

Pay down existing debt, especially revolving debt like credit cards. This will help improve both your DTI and your credit utilization ratio. Pay all bills on time every month. Late or missed payments appear as negative information on credit reports.