What are the qualifications for down payment assistance?

Robert Bradley

Robert Bradley

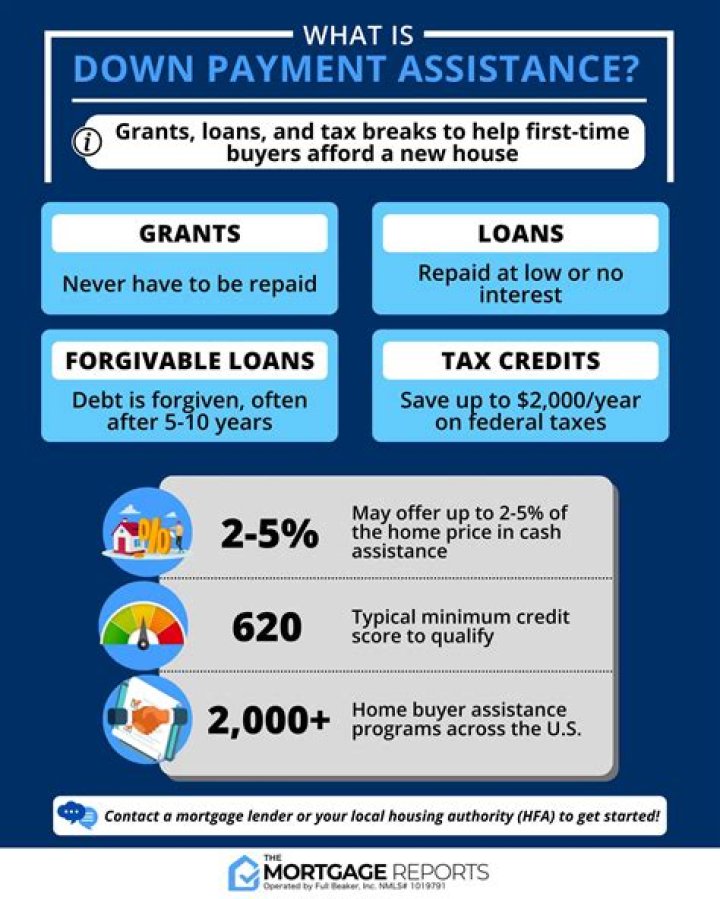

Who qualifies for down payment assistance?

- Restricted to first-time home buyers.

- Buyers often must have low- to moderate-income.

- The buyer is using the home as their primary residence.

- The home is in a “targeted” census tract.

- The DPA is used in conjunction with an approved mortgage program.

How can I buy a HUD home with no money down?

Although there are no government programs offering no money down, HUD houses can be purchased using the federal lender, the Federal Housing Administration (FHA), which offers a $100 down program. In order to qualify, the home must be owner-occupied, meaning the purchaser lives in the home.

Can you qualify for more than one down payment assistance program?

Can you use multiple down payment assistance programs? Yes again, although it depends on what programs you hope to bundle. For example, you can combine a family gift with a low down payment loan. If you qualify for a VA loan, you won’t need a down payment.

Can a HUD partial claim be forgiven?

The FHA works with approved lenders in the United States and agencies such as the U.S. Department of Housing and Urban Development (HUD) to offer HUD partial claim forgiveness. Homeowners can fall behind on their loan payments, and these options may help those who are struggling.

How can I get my house down payment fast?

Potential homeowners can come up with the down payment by getting a part-time job or borrowing from family. Downsizing to a smaller apartment—saving rent—can save thousands of dollars per year. Programs can help, such as the Federal Housing Administration (FHA), which offers mortgage loans through FHA-approved banks.

What is the minimum down payment on a house?

FHA loans, backed by the Federal Housing Administration, are available for as little as 3.5 percent down if the borrower has a credit score of at least 580. If the borrower has a lower score (500-579), the minimum down payment is 10 percent.

Is it hard to get approved for a HUD home?

HUD is not a lender for homes. Anyone with the cash or an approved loan can qualify for a HUD property. For FHA-insured properties, buyers can qualify for FHA financing with only 3.5 percent down with a minimum credit score of 580. HUD and FHA are not lenders.

Can closing costs be included in loan?

Including closing costs in your loan or “rolling them in” means you are adding the costs to your new mortgage balance. This is also known as financing your closing costs. Financing your closing costs does not mean you avoid paying them. It simply means you don’t have to pay them on closing day.

Do you have to pay back HUD?

Funding for the program comes primarily from the Department of Housing and Urban Development. HUD gets the money it needs from the taxes people pay to the government. As a public, tax-funded program, Section 8, like other forms of welfare, does not require repayment.

Can you get a FHA loan for a down payment?

Funded by the CBC Mortgage Agency, this program offers the ability to utilize an FHA-insured home loan by offering eligible applicants 3.5% of the purchase price to cover the down-payment. The assistance funds come in the form of a zero-interest second mortgage with a 30-year term.

Is there a HUD 100 down payment program?

The HUD $100 down program is an FHA loan with a twist. Instead of the minimum required 3.5% of the price down payment, FHA allows a $100 minimum required investment. Regretfully, this program is limited to eligible properties. In order to use the HUD $100 down program, the property must be a HUD foreclosure or in other words, a HUD REO.

Is there a HUD down payment for first time home buyers?

Check out the chart below or click the link to search your county. Many buyers, especially first time home buyers, are looking for as little down payment as possible. Well, $100 is pretty low! The HUD $100 down program is an FHA loan with a twist.

Can a HUD loan be used for a foreclosure?

Many foreclosures need renovations and HUD foreclosures are no different. Often, foreclosures are vacant for a period which means they may be neglected. Luckily, an FHA 203k loan will finance the purchase and renovation of a home. There are many great benefits of the 203k renovation loan. First, there is still only a 3.5% down payment.