Is it normal for your credit score to drop after paying off debt?

Sarah Duran

Sarah Duran

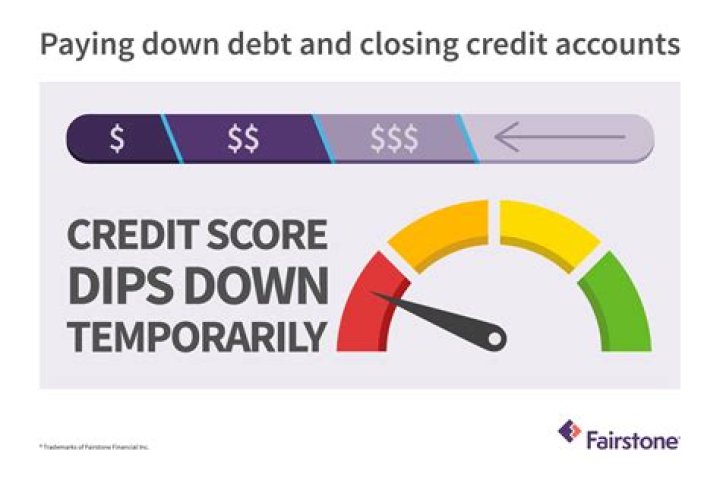

Paying off a credit card doesn’t usually hurt your credit scores—just the opposite, in fact. It can take a month or two for paid-off balances to be reflected in your score, but reducing credit card debt typically results in a score boost eventually, as long as your other credit accounts are in good standing.

How long does it take to get your credit score up after paying off debt?

Usually, creditors inform credit activities to credit bureaus once per month. So after you repay the debt, your FICO score may increase within 2 billing cycles. Keep in mind that paid off accounts stay on credit report for 10 years. Even if you pay off all debts at once, the missed payments will appear on your credit report for 7 years.

How long does it take to get a collection off your credit report?

Paying off a collection account is a good idea for several reasons—but the account won’t fall off your credit report just because it’s paid. A collection account—paid or unpaid—remains on your credit report and visible to potential creditors for seven years from the date of the first missed payment on the debt in question.

What happens to your credit report after seven years?

Your credit report, if you’re not familiar, is a document that lists your credit and loan accounts and payment histories with various banks and other financial institutions. The seven-year mark does not erase the actual debt, particularly if it’s unpaid.

How does paying off debt affect your credit report?

If you can afford to pay the debt anyway, it will be marked on your credit report as “satisfied.” This won’t improve your credit score, but a lender looking at your report might be more willing to trust you because you made the effort. Our Editor Sam Robson has been on a personal cost-cutting mission for years – and it’s time to share his wisdom.