Is it better to pay off a student loan or make payments?

James Rogers

James Rogers

Paying off your loans early means making additional payments or larger payments, so you should only increase your student loan payments if you can afford to do so without making undue sacrifices. You’re better off making your required payments until the debt is forgiven.

Is it a bad idea to borrow money to pay for college?

if your plans are to borrow money to help them pay for college, you’re likely making a very costly mistake. if your plans are to borrow money to help them pay for college, you’re likely making a very costly mistake.

Is it better to pay off student loans quickly or over time?

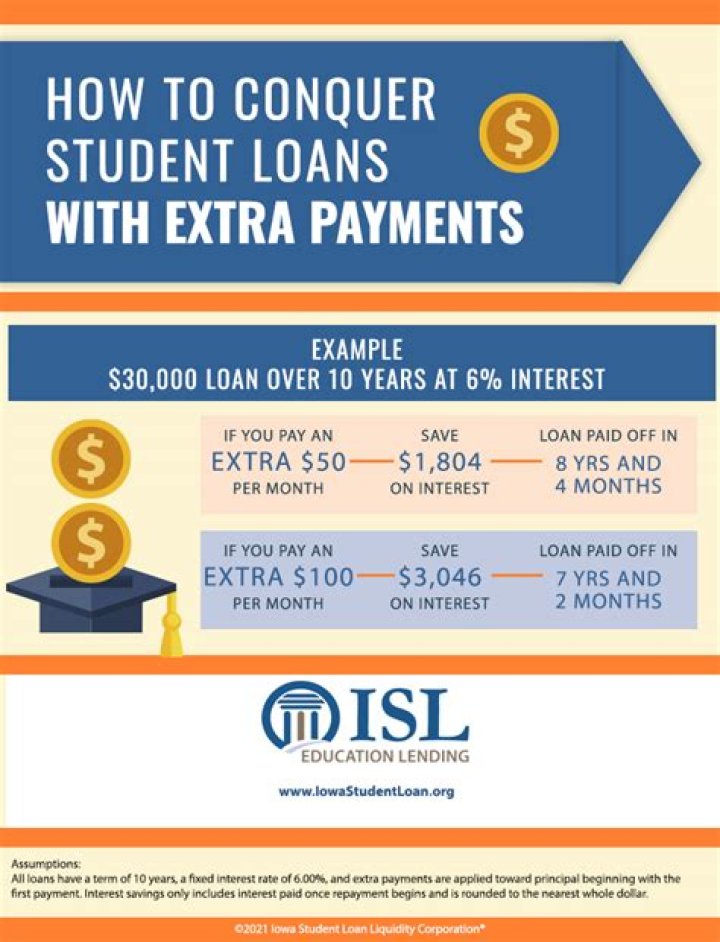

Yes, paying off your student loans early is a good idea. Paying off your private or federal loans early can help you save thousands over the length of your loan since you’ll be paying less interest. If you do have high-interest debt, you can make your money work harder for you by refinancing your student loans.

Is it worth it to take out student loans?

Student Loans Are Worth It If You Have a Solid Plan Depending on your selected major and financial situation, the answer is often yes. However, take out the smallest amount of federal and/or private student loans possible to pay for your program to make it easier to manage your loans after you graduate.

Why are students loans bad?

Plus, the high amount of debt compared to a lower salary can produce a skewed debt-to-income ratio, which can hurt your credit. Unaffordable student loan debt can lead to delinquency and even default, which can ruin your credit score and prevent you from getting approved for other types of credit.

How much money should I borrow for college?

That leaves many students wondering how much money they need to borrow to pay for college. While there’s no set number for everyone, most financial experts say students should borrow no more than $5,000 a year.

Does paying off a student loan early hurt your credit score?

If you choose to pay student loans off early, there should be no negative effect on your credit score or standing. However, leaving a student loan open and paying monthly per the terms will show lenders that you’re responsible and able to successfully manage monthly payments and help you improve your credit score.

What can I do with a year off before college?

Many students decide to take a year off to travel abroad but some choose to work either as an intern or part- or full-time employee. Those who take this route, can put their paychecks towards their college education.

Why does it cost more to borrow than to save?

The difference between the rate at which it borrows money from you (the savings rate) and the rate it charges others (the borrowing rate) is its profit. Therefore, on the whole, it’ll always cost more to borrow than you can earn by saving.

Is it better to save money or pay off debts?

As a raw answer yes. It’s generally worth having three to six months’ worth of expenses put aside in savings in case of an emergency. Certainly for loans, mortgages and other fixed repayment borrowing.

How to pay off the most expensive debts first?

Pay off the most expensive debts first 1 For credit and store cards, read Best Balance Transfers. 2 If you get rejected for new credit then you can still cut rates using The Credit Card Shuffle. 3 If you have a loan read Cut the Cost of Existing Loans. 4 For cutting costs on your mortgage read the Remortgage Guide.