How much does your credit score drop when you buy a car?

Sebastian Wright

Sebastian Wright

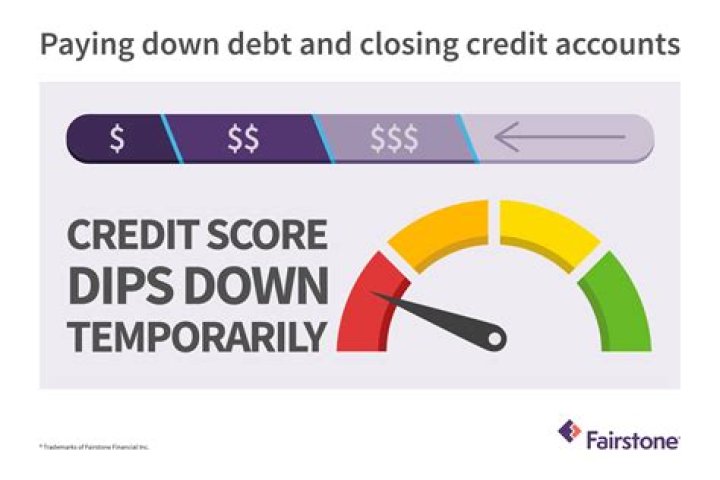

Each credit report the auto loan lender pull adds 1 new hard inquiry, and each hard inquiry lowers your score up to 10 FICO points. A single car loan application could lower your score up to 30 points.

Does your credit go down when you buy a new car?

When you first get an auto loan, you may see a slight dip in your credit scores because you’re taking on a hefty new debt. However, as you begin making on-time payments on the loan, your credit score should bounce back. Buying a car can help your credit if: You make all of your payments on time.

Do dealerships lower your credit score?

The truth is, the dealers don’t really care about the score that you can readily show them on your phone because it’s not the same thing as the score they will pull when they run your credit because they operate on different credit scoring models. Here is a closer explanation of what we mean.

What happens when you buy a new car with a low credit score?

That is largely affected by your credit score. If you have a low credit score, then your interest rate will be high and that will increase your monthly payments significantly. If it’s going to be tight, your best bet is to focus on improving your credit score first, before buying a new car.

How does a car loan affect your credit?

The long-term effect of a car loan on your credit score isn’t all bad, however, First, your payment history counts for 35 percent of your credit score, so making your monthly payments on time every month gives your score a boost.

What’s the average credit score to buy a car?

Borrowers with 500 or lower saw an average rate as steep as 20%. Overall, car buyers had an average credit score of 717 on loans and leases for new cars and 656 on loans for used vehicles, according to Experian. Data crunched by U.S. News & World Report in October 2019 slices it a bit differently.

What’s the average loan for a new car?

After all, for many of us, a loan to buy a car or truck will be one of our largest loans. Most of us (84%) rely on financing when purchasing a vehicle, according to data from Experian Automotive (fourth quarter, 2014) and the average loan amount for a new vehicle is $28,381; the highest on record and an increase of almost $1,000 from a year ago.