How do you get out of a personal guarantee on a commercial loan?

Elijah King

Elijah King

You can ask to be relieved of the personal guarantee after a certain percent of the loan has been repaid or your share in business has been sold. Modify the reporting requirements. Lenders typically require guarantors to submit personal financial information at least annually.

What happens to business debt in bankruptcy?

In a Chapter 7 bankruptcy, your assets (except for property that’s exempt under state or federal law) can be sold to pay off your creditors. At the end, all your debts that are eligible for discharge in bankruptcy will be wiped out.

How do you get out of a personal guarantee?

Obviously, repayment is one way to release yourself from a personal guarantee on a loan for your business. You may also be able to renegotiate the loan with your bank, asking them to remove your personal guarantee based on the company’s assets and performance.

What is an unsecured personal guarantee for a loan?

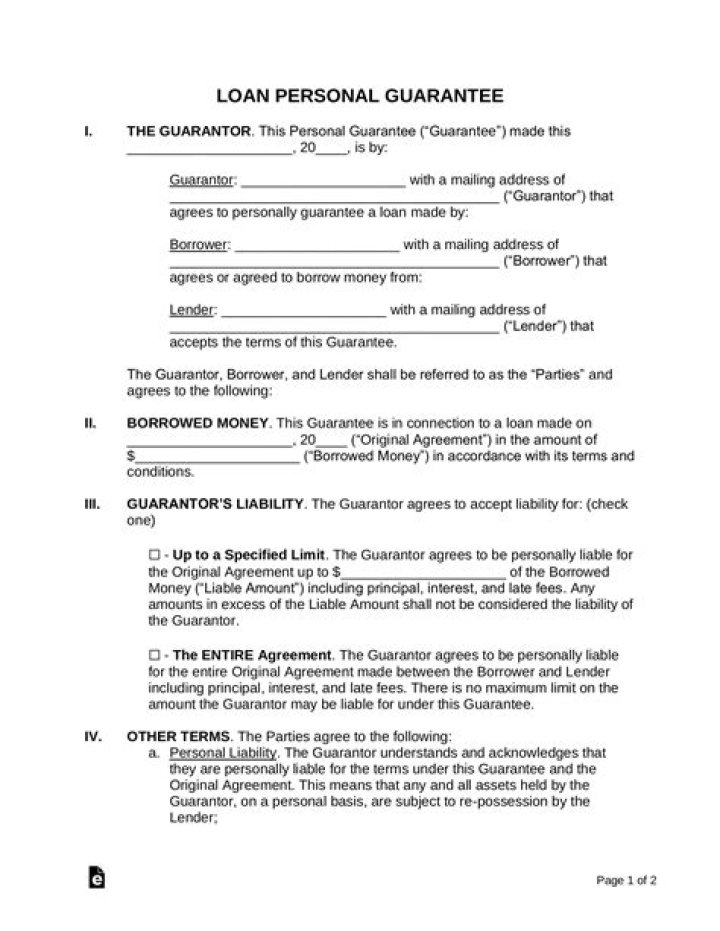

A personal guarantee is an unsecured written promise from a business owner and or business executive guaranteeing payment on an equipment lease or loan in the event the business does not pay. Since it is unsecured, a personal guarantee is not tied to a specific asset.

Can a personal guarantee be wiped out in bankruptcy?

When you personally guarantee a loan for your business, friend, or family member, you make yourself liable for it. Luckily, you can usually wipe out your personal liability for debt through bankruptcy—including a personal guarantee for your business. Read on to learn more about how you can eliminate a personal guarantee through bankruptcy.

Can a business owner get rid of a personal guarantee?

It’s relatively common for a business owner to file individual bankruptcy to get rid of a personal guarantee—and most personal guarantees will qualify for discharge. If it’s a nondischargeable debt, however, bankruptcy won’t help.

What happens when a company files personal bankruptcy?

When a business fails to pay (or shuts its doors), the lender will pursue the personal guarantee, often leaving the signer of the guarantee with one of two options: pay the company debt out of individual assets, or, if the signer doesn’t have the funds, file a personal bankruptcy. Learn more about the lasting effects of a business bankruptcy.

When is the best time to file personal guarantees bankruptcy?

If you don’t have much in the way of income or property—primarily debt— Chapter 7 will likely be your best option. You can wipe out (discharge) qualifying debt, such as credit card debt and personal guarantees, in approximately four months.