Does PMI protect the borrower?

Aria Murphy

Aria Murphy

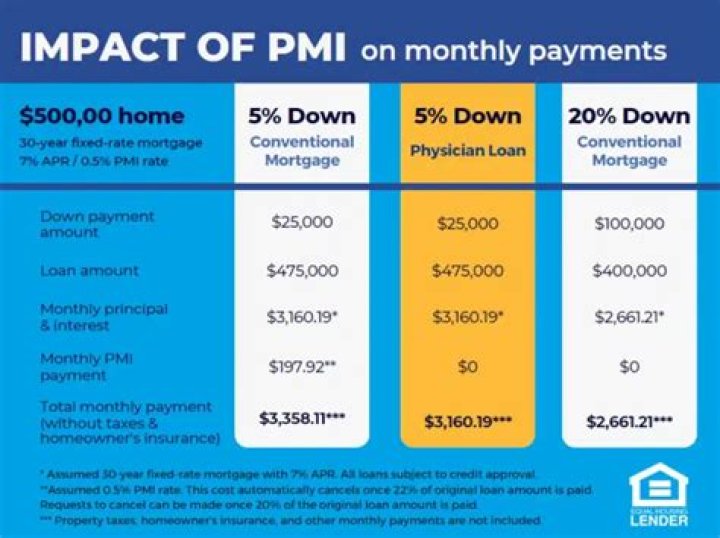

Private mortgage insurance, also called PMI, is a type of mortgage insurance you might be required to pay for if you have a conventional loan. Like other kinds of mortgage insurance, PMI protects the lender—not you—if you stop making payments on your loan.

Do you never get PMI money back?

Lender-paid PMI is not refundable. The benefit of lender-paid PMI, despite the higher interest rate, is that your monthly payment could still be lower than making monthly PMI payments. That way, you could qualify to borrow more.

Does PMI pay off mortgage upon death?

PMI stands for private mortgage insurance. However, PMI doesn’t pay off your loan if you die. In fact, it is intended more as a protection for your lender if you don’t repay your debt. Mortgage protection insurance is an option if you want this type of death benefit.

How to make your mortgage payments after bankruptcy?

1 Chapter 7 Bankruptcy and Your Mortgage. If you file (and qualify) for Chapter 7 bankruptcy and your home is exempt, you can continue to make your mortgage payments if you 2 Chapter 13 Bankruptcy and Your Mortgage. 3 Modifying Mortgages: Cram Down in Bankruptcy. 4 Getting Your Lender to Modify Your Home Loan. …

How are mortgages discharged in Chapter 13 bankruptcy?

Just like medical or credit card debt in Chapter 13, you don’t have to make payments on this debt outside of your bankruptcy. Instead, you will pay a portion of this unsecured debt (usually a very small amount) through your Chapter 13 plan. If you complete the plan, anything left on the mortgage is discharged (wiped out).

Can You Keep your mortgage if you file Chapter 7 bankruptcy?

The bad news is that some homeowners filing for Chapter 7 bankruptcy will lose their home. In Chapter 13 bankruptcy, you can keep your home and continue with your current mortgage. If you file (and qualify) for Chapter 7 bankruptcy and your home is exempt, you can continue to make your mortgage payments if you want to keep your home.

Can you get an FHA loan with Chapter 13 bankruptcy?

FHA loan with Chapter 13 bankruptcy To qualify for an FHA loan during Chapter 13, you need to be at least 12 months into your repayment plan. And you must have made all those payments on time. In addition, the bankruptcy court or bankruptcy attorney needs to give written permission for you to take out a new mortgage loan.