Does bankruptcy protect you from a personal guarantee?

Aria Murphy

Aria Murphy

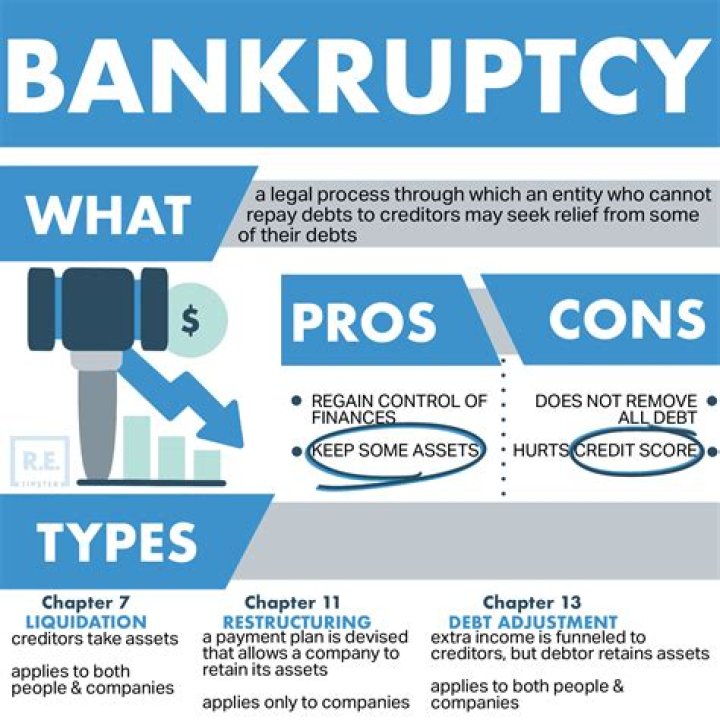

It’s relatively common for a business owner to file individual bankruptcy to get rid of a personal guarantee—and most personal guarantees will qualify for discharge. If it’s a nondischargeable debt, however, bankruptcy won’t help. You’ll have to file individual bankruptcy to get rid of the obligation.

Does a personal guarantee show on credit report?

Personal guarantees don’t have a direct impact on your personal or business credit history, or credit score unless you run into trouble. “They don’t typically show up on credit reports,” Luebbers says. But, a personal guarantee could affect your credit if you have late payments or default on the loan.

Can a personal guarantee be wiped out in bankruptcy?

Because your business was new, the bank asked you to execute a personal guarantee. By signing the guarantee, you agreed to use your personal assets to pay off the loan if the business was unable to do so. If the cupcake business dried up and the bakery closed, you’d likely be able to wipe out the guarantee in Chapter 7 or Chapter 13 bankruptcy.

Can a business file for Chapter 7 bankruptcy?

Such owners are personally responsible for both individual and business debts, and therefore, a bankruptcy filing will include all obligations (and all nonexempt assets, as well). As a result, a Chapter 7 bankruptcy will wipe out both the underlying business debt and the individual liability under a personal guarantee.

Can a personal guarantee prevent you from filing Chapter 7?

The means test prevents many people from filing for Chapter 7. However, when most of your debt is business-related as opposed to consumer debt, you aren’t subject to the Chapter 7 means test income qualification. This can be a huge benefit for someone with a personal guarantee liability.

What happens when a company files personal bankruptcy?

When a business fails to pay (or shuts its doors), the lender will pursue the personal guarantee, often leaving the signer of the guarantee with one of two options: pay the company debt out of individual assets, or, if the signer doesn’t have the funds, file a personal bankruptcy. Learn more about the lasting effects of a business bankruptcy.