Can you HELOC a foreclosure?

Robert Bradley

Robert Bradley

If you are unable to repay a loan that was secured by your home, such as a home equity line of credit, or HELOC loan, California law generally allows the lender to foreclose on your home to collect the loan.

Can you use a HELOC to pay off a second mortgage?

Is a HELOC Your Best Option for Paying Off a Mortgage? The short answer to this question, is no. Technically, you can use the money in your HELOC for anything: renovations, vacation, car, tuition, etc. But using a HELOC to pay down your mortgage isn’t a sound financial idea.

Can you use home equity to pay closing costs?

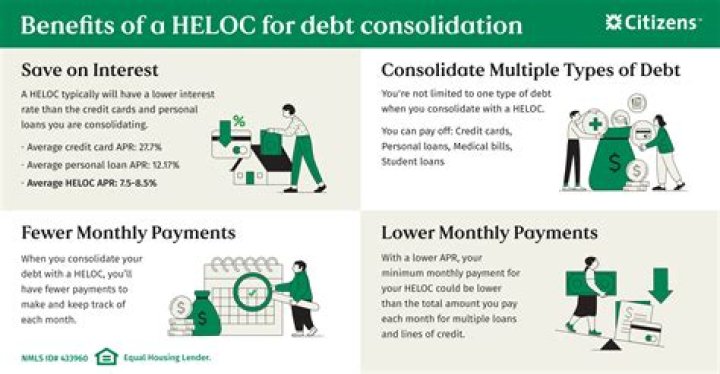

Home equity loan closing costs can range from 2% to 5% of your loan amount. A home equity loan allows you to borrow a lump sum against your available equity, and can help you cover home improvements, pay college costs or consolidate high-interest debt.

Can I remortgage my house if I own it?

Can I remortgage if I own my house outright? People who have no mortgage on their home, (known as an unencumbered property) are in a strong position to remortgage. With no outstanding mortgage, you own 100% of the equity in your house. You will need to meet the criteria for the new mortgage.

How soon after closing can you get a home equity loan?

30 to 45 days

If you have enough equity at the time of closing your home purchase, you can get a HELOC in as little as 30 to 45 days, which is the time it takes for loan underwriters to process the application. They use this time to confirm you meet lending requirements for the new debt.

Can a home equity line of credit be used for a second mortgage?

Make sure you’re able to pay a second mortgage on top of the mortgage you’re already paying. Plan carefully and talk to your financial adviser to see if a second mortgage makes financial sense for you. Home equity loans or second mortgages are different than a home equity line of credit (also called a HELOC).

Can a HELOC be used to pay off a mortgage?

Using a HELOC to pay off a mortgage is simple. Assuming you can get approval and have enough in equity, you simply borrow the balance of your mortgage and send it to the lender. The process is best suited for a homeowner who: Or has enough equity to also make some improvements on the home.

When do you have to pay off a home equity loan?

Often, you have to pay off a home equity loan or second mortgage within about 15 years, though the terms vary. The interest rate on the loan is typically fixed.

What to do with money from second mortgage?

Homeowners may use the money from these second mortgages – available as a lump sum home equity loan or as a home equity line of credit – for any purpose. Deciding which loan is right for you depends on the loan’s purpose and your personal spending habits.