Can I get a USDA loan with collections on my credit report?

Emily Carr

Emily Carr

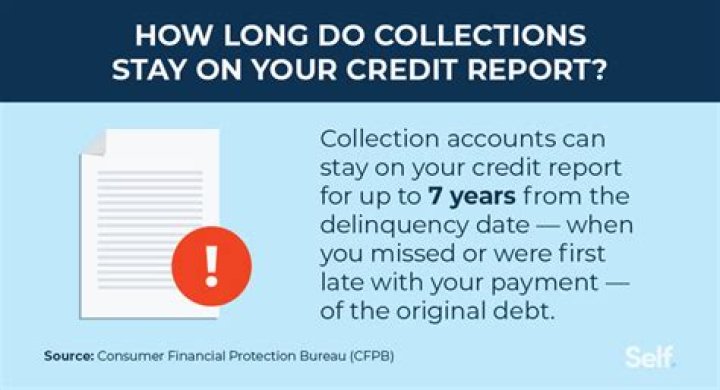

Tim: Yes, you can still get approved for a USDA loan after paying off collections or making arrangements to pay them. However, paying off collections can actually make your credit scores go down since that makes the collection accounts look new. The USDA website says that there is no minimum credit score limit.

Does USDA run your credit?

While the USDA doesn’t have a set credit score requirement, most lenders offering USDA-guaranteed mortgages require a score of at least 640. This is the minimum credit score you’ll need to be eligible for automatic approval through the USDA’s automated underwriting system.

Does USDA require 2 year work history?

USDA encourages lenders to review the previous two year employment history for each applicant, however most income types require a minimum of 12 months on the job to be considered for repayment purposes. Applicants who have less than 1 year of employment history are not considered to have stable or dependable income.

Which credit report does USDA use?

FICO scores are judged on a 300-850 score range. The higher the score, the lower the risk. Each CRA will give you a slightly different score regardless of which credit score you use. When evaluating you for a USDA loan, lenders will generally choose the middle of the three scores.

Is it hard to get approved for USDA?

Qualification is easier than for many other loan types, since the loan doesn’t require a down payment or a high credit score. Homebuyers should make sure they are looking at homes within USDA-eligible geographic areas, because the property location is the most important factor for this loan type.

What are the cons of a USDA loan?

The Possible Drawbacks

- Only primary residences can be purchased. USDA loans cannot be used to purchase a vacation home or rental property.

- There are geographical restrictions. Homes in urban centers won’t qualify.

- There are income limits.

- Mortgage insurance is factored into the cost.

What disqualifies a home from USDA financing?

1. Income and debt issues. Things like unverifiable income, undisclosed debt, or even just having too much household income for your area can cause a loan to be denied. Talk with a USDA loan specialist to get a clear sense of your income and debt situation and what might be possible.

What FICO score does USDA loans use?

a 640 FICO score

USDA loans are popular for their zero down payment requirement and low rates. You’ll typically need a 640 FICO score to qualify for a USDA loan, though minimum credit score requirements vary by lender.

Do USDA loans take longer to close?

The entire USDA mortgage closing time will take about 35 days on average from contract to closing. Some less populated states are faster. Sometimes things come up in the process that can add small delays to the process. Buyers should remember there are MANY moving parts to a real estate transaction.

How long does it take to close on a USDA loan?

Buyers considering a USDA loan often want to know how long it takes to close on a USDA loan. Every homebuying situation is different. But once you’re contract to purchase, you can typically expect the USDA loan process to take anywhere from 30 to 45 days to close on your USDA loan.

How are credit scores evaluated for a USDA loan?

The main aspects of a credit report that is evaluated to determine borrower eligibility for USDA loans are credit scores and credit history.

What do I need to get a USDA loan?

Additionally, you must be able to show at least 3 trade-lines on your credit report, such as credit cards or auto loans. If you do not have sufficient trade-lines on your credit report, you may still qualify with alternative forms of credit, such as phone bill, utility payments, or even a gym membership.

Are there exceptions to USDA loan credit requirements?

There are few exceptions to this rule, which one may still be able to obtain financing. This includes an “extenuating circumstance”, such as temporary job loss, illness, or other matters which may have been out of ones control and resulted in the foreclosure.