Can a private student loan be discharged in bankruptcy?

Emily Carr

Emily Carr

Except in rare situations, bankruptcy law states that neither federal loans nor private student loans are eligible for a bankruptcy discharge. To discharge a student loan in bankruptcy, you must file an adversarial proceeding (AP). An AP is a lawsuit filed within the bankruptcy court, after a bankruptcy case has already been filed.

How to get rid of private student loans?

You must do two things to file bankruptcy on private student loans: file a Chapter 7 bankruptcy or Chapter 13 bankruptcy and file an adversary proceeding to discharge your private student loan debt. Filing bankruptcy will eliminate your consumer debt (unsecured debt and secured debt).

How can I discharge my student loan debt?

To discharge student loan debt in bankruptcy, you have to first file a bankruptcy case and then file an adversary proceeding. The adversary proceeding is the name given to lawsuits in bankruptcy proceedings. You can file the AP before your bankruptcy case ends. You can also file it after you’ve gotten a bankruptcy discharge.

Can a federal student loan be used for a private loan?

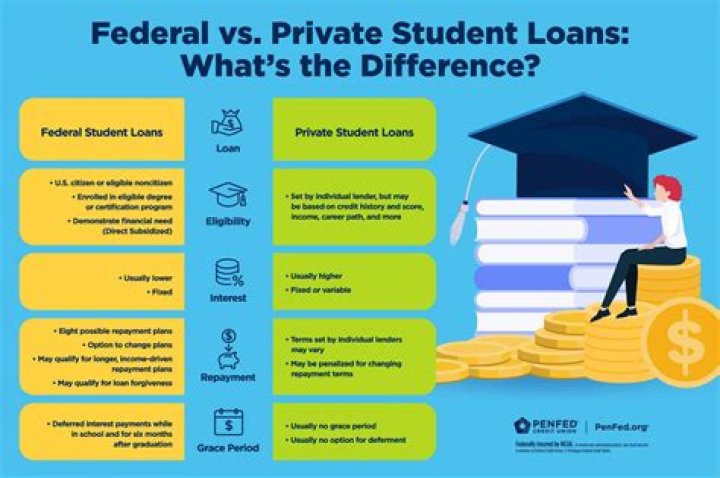

Private student loans are loans extended by private lenders that are not backed by the federal government. These loans are only to be used for qualified educational expenses. Private student loans don’t have many of the relief provisions allowed for by federal student loans.

What kind of bankruptcy do you need for student loans?

Chapter 7 bankruptcy. In Chapter 7 bankruptcy, if payment of your loans is not an undue hardship, you’ll still owe them when your bankruptcy case is over. Chapter 13 bankruptcy. If you can’t discharge your student loans, Chapter 13 bankruptcy provides some other ways that can help.

How can I get my student loan discharged?

To find out the test used in your jurisdiction, talk to a local bankruptcy attorney. If you want to try to discharge your student loan in bankruptcy, you must file an adversary proceeding to determine dischargeability with the bankruptcy court. But that’s not all.

How can I get rid of my private student loan?

The best way to reduce or eliminate your private student loans might be a debt settlement. It would be rare for a debt settlement company to attempt to negotiate a settlement for a private student loan. But, there are some student loan attorneys that specialize in such settlements.

Can a cosigner be liable for debt if I file bankruptcy?

Your bankruptcy discharge only eliminates your obligation to pay discharged debts. It doesn’t affect the responsibility or liability of the cosigners and guarantors on your debts. However, how much protection they will receive when you file depends on whether you file a Chapter 7 or Chapter 13 bankruptcy.

What happens if you cosigned a student loan?

Unfortunately, a cosigner in student loan default might not know there’s a problem until the loan has already defaulted. In this case, the lender or debt collectors will start pursuing you for repayment or send the debt to collections. And the consequences can be big.

Can a creditor pursue a cosigner at any time?

For instance, a creditor can pursue a cosigner at any time. But with guarantors, creditors usually must attempt to collect from the primary borrower first before going after the guarantor. The guarantor must make the lender whole (pay off the loan) if the borrower can’t do so.